So you want to... be debt free?

By MAS Team | 31 July 2019

By MAS Team | 31 July 2019

Last updated July 12, 2022.

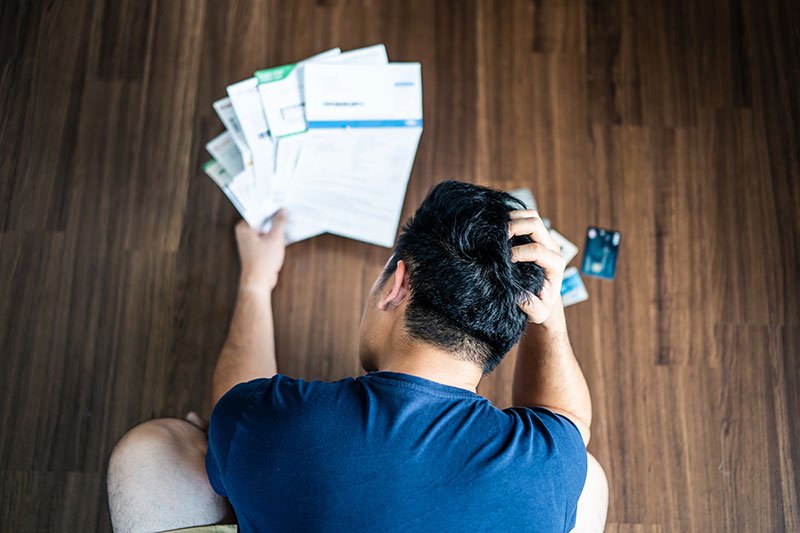

Student loans, overdrafts, credit cards, personal credit lines – debts can feel like a dark cloud hanging over your head.

Taking control of your debts and making an action plan to tackle them will feel like a weight lifted off your shoulders, so find out more about how to be debt free.

Setting up a budget is the first step to taking control of your finances. There are lots of tools and spreadsheets out there to help you manage your income and costs – this budgeting tool by Sorted is really helpful. Setting up a budget is a worthwhile thing to do as it will help you see where your money is going and where you could save a few dollars. If you’re a MAS Member, head to our Āki health and wellbeing portal and check out our Money Talks challenge for some practical step-by-step advice on shredding that debt.

While paying off debts is a priority, it’s also important to make sure you still have enough for all your living costs as well as the occasional brunch date or trip to the movies. The best budget is one you’ll stick to, so be realistic.

If you have any high interest-earning debts, such as overdrafts and credit cards, paying them back as quickly as you can should be your first priority. Paying them back fast means your overall debt won’t keep growing with the interest being charged on them. Make sure you’re meeting at least the minimum repayments as often there are penalties for not doing so, and if you have any extra money you can use this towards faster repayments, which will help you get your balance under control.

Have a read of our guide what to know about credit cards to find out more about tackling your personal debt.

Your student loan may look big and scary, but the positive is that this loan is interest-free as long as you live in Aotearoa New Zealand. You can chip away at it with the minimum repayments required and not think about it until you’ve got your other debts under control.

Of all debts, student loans are fairly easy to manage as deductions happen automatically once you start earning $21,268 or more a year. When you have squashed all other debts, then consider ramping up your student loan repayments. Check out our tips for paying off your student loan.

If you’re one of the many Kiwis who choose to work overseas for a few years, or even travel for an extended period of time, make sure you’re aware of the impact this will have on your student loan balance.

Once you’re out of the country for about five months out of a six month period, you might be considered ‘overseas based’ and your student loan may start to accrue interest. With interest building up, your student loan will grow bigger and you will be required to make minimum repayments, unless you arrange a temporary payment suspension. Find out more about your obligations for repaying your student loan while overseas.

It’s easy to stick with the same provider for years, but when you shop around, you can often find cheaper deals for power, mobile, broadband and insurance. Compare different companies to check if they are giving you the best value, as well as looking at their service and social impact. You might be able to save money and have a positive impact at the same time.

Do you ever wander around the supermarket aisles aimlessly and end up buying far too much food? Aim to plan your weekly meals ahead of time. Do some meal planning in advance, be conscious of what’s on special, and take a list to the supermarket. You could even consider doing your grocery shopping online to help you stick to purchasing only what you need – as well as saving petrol and your time. Also, make sure you’re shopping in season – cucumbers are tasty but are they really worth $6 in winter, compared to $1.50 in summer?

Buying in bulk can be worth it, but be smart about it – purchasing three packs of chips for $5 will just mean eating more chips, but buying household items like toilet paper or washing powder in bulk can be worth it.

Paying off debts is no easy feat, so remember to treat yourself when you meet your targets and milestones. When you reach those goals, reward yourself with a celebratory lunch or something small to keep you motivated on your journey to becoming debt-free.

We all need a bit of fun in our lives – just remember not to take it too far, as you don’t want to end up back in serious debt that you worked so hard to get out of. Have a read about how one MAS Member found a balance between saving hard and enjoying life after graduating.

Have a chat with a MAS Adviser today to find out more about becoming debt-free.

This article provides general information only, and is not intended to constitute financial advice.

14 April 2021

If you're planning on buying a home in the future, good news – KiwiSaver can also be used by first-home buyers to get on the property ladder. Here's what you need to know to get the most out of KiwiSaver.

24 September 2019

The oldest Baby Boomer in the flower-power generation bracket is 72, while the youngest members of Generation Z are just four years old. The money habits and priorities between these generations are very different.

10 January 2023

Figuring out exactly how much contents insurance cover you need can be difficult. Here’s our guide to how much contents insurance you need, and how to make sure you’re covered if the worst happens.