The EQC and Your House Insurance Policy

By Dawn Chapman | 7 September 2021

The Earthquake Commission (EQC) provides natural disaster insurance for residential homes and certain areas of residential land in New Zealand.

You automatically have EQC cover if you have a current private house insurance policy that includes fire insurance. Part of the premium you pay for your house insurance is made up of an EQC levy, which we collect on EQC’s behalf.

EQC insures your home against certain types of damage caused by events including earthquakes, natural landslips, volcanic eruptions, tsunamis, or hydothermal activity.

As well as your home, EQC also covers residential land, within limits, for the same events, as well as against storm and flood damage. Damage to your house and contents from storms or floods is covered by your private insurance.

The EQC also covers fire damage resulting from any of these types of natural disaster.

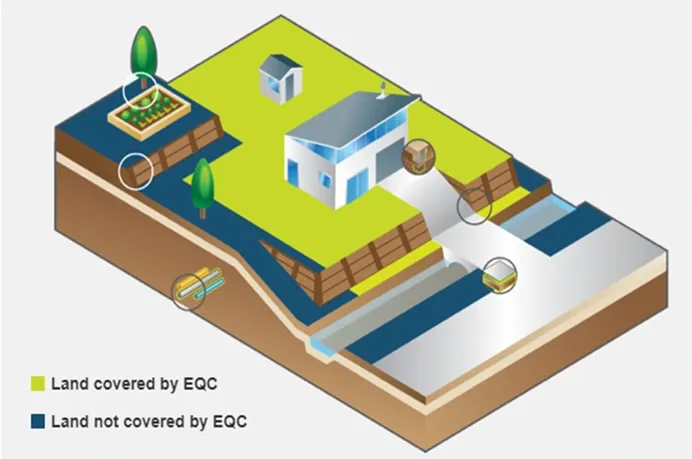

EQC insures:

EQC covers damage to land within your property boundary, including:

EQC also provides some cover for:

Certain items on the land such as trees, plants, lawns and driveways aren’t covered by EQC.

In 2019, EQC stopped providing cover for damage to contents. If you took out a contents policy after 2019, or renewed your contents policy after that date, your contents are not covered by EQC.

In these cases, your MAS contents policy provides cover for damage that has occurred to your contents.

If you need to make a claim for natural disaster damage, EQC will cover a portion of your loss, up to a capped amount.

For damage to your home, your claim will be covered by the EQC up to $150,000 (+GST), per dwelling. If the damage is more than this capped amount, MAS covers the rest.

The amount you can receive for damage to residential land is assessed in a slightly different way. EQC will cover either the value of the damaged land or the cost to repair the damage land, whichever is the lesser amount. These amounts are determined by an assessor and other specialists.

EQC also covers bridges, culverts and retaining walls that support the home or insured land. The amount you receive will be the cost to repair them to the state they were in before the loss or damage occurred. This means that the valuation will take into account their age and previous state of repair.

MAS house insurance policies do not include cover for land damage. However, if your claim is accepted by EQC, we may provide some limited cover for driveway resurfacing and top-up cover for retaining walls.

If you need to make a claim and you hold a current house insurance policy with MAS, we manage your entire claim from lodgement to settlement. This includes managing claims for any EQC-covered damage on your behalf.

You can lodge your claim online with MAS or phone us on 0800 800 627.

If your claim is accepted by EQC, you will need to pay an excess, which will be deducted from your claim settlement.

For damage to your home, this is 1% of the amount payable for the claim, with a minimum excess of $200. The maximum excess you will pay for your EQC Home claim is $1,725 per dwelling.

You may also need to pay a separate excess for an EQC Land claim, even if it’s related to the same event. This is 10% of the amount payable for the claim, with a minimum of $500 per dwelling on the land. The maximum excess you will pay for your EQC Land claim is $5,000.

There will also be an excess you need to pay on claims you make against your MAS policy for damage that is not covered by the EQC Act.

24 September 2019

The oldest Baby Boomer in the flower-power generation bracket is 72, while the youngest members of Generation Z are just four years old. The money habits and priorities between these generations are very different.

28 September 2022

If you think you might need life insurance, the process for getting it is pretty simple. Here’s a step-by-step breakdown of getting life insurance with MAS.

27 October 2020

The MAS KiwiSaver and Retirement Savings Plan funds invest in Afterpay, and we had a chat with Tom Phillips from investment manager JBWere, about why the stock has performed so well in 2020.